Value of Brazilian Beef Sales to Ei

Note: This report includes forecasting data that is based on baseline historical data.

Executive summary

In 2020, South American markets imported a total of US$313.3 million from the world in dog and cat food products, put up for retail sale. Top countries for trade in this region included Chile (US$112.2 million), Colombia (US$67.8 million), and Uruguay (US$38.2 million).

Brazil, Argentina, and Venezuela currently are not an import trading partner with Canada in the pet food sector, however, all three emerging markets have high demand for pet food products due to their large pet population and high retail sales values. Brazil is one of the main pet markets in the world and leads in the South American market at a retail sales value of US$4.4 billion in 2020. Argentina was South America's fourth largest retail market with a sales value of US$742.5 million and Venezuela ranked sixth largest at US$102.0 million.

These selected markets have faced economic crisis' over the last 3 to 4 years. Venezuela has the world's highest inflation, with the non-official rate reaching as much as 2,600% in 2017 (Euromonitor, 2018). This has affected consumer spending habits in several sectors, yet as pet humanisation is a valued global trend, there exists a growing demand for pet food product premiumisation. Brazilian pet owners are the most willing to purchase mid-priced brands with premium positioning, while Argentina and Venezuela remain more cautious and prefer more economy-priced brands. Albeit, once economic recovery occurs in these markets high growth is expected in the retail pet food sector (more in value over volume sales) up to a compound annual growth rate (CAGR) of 28.8% (particularly in Argentina) by 2025.

In 2020, traditional grocery retailers was the largest distribution channel in Argentina, while non-grocery specialists like pet shops were more popular in Brazil. Growing and essential retailer outlets included mixed retailer club warehouses, along with non-retail veterinary clinics that are preferred pet care outlets to gain specialized advice, insights and knowledge. Non-store e-commerce retailing is a growing pet food channel, doubling in sales distribution share in both markets (2020/2019).

Sector overview: Pet population and ownership

In 2020, the Brazilian pet population was around 212.6 million, equivalent to 67.3 million households who are pet owners (includes dog, cat, bird, fish and small mammal/reptile). More households own a dog at a population of 33.0 million (49.0%) over a cat at 14.3 million (21.2%) households in Brazil. The number of households owning pets has increased at a CAGR of 1.3% with it's population of pets increasing by 0.8% (2016-2020). The number of households with pets are expected to increase by a CAGR of 0.9%, equivalent to a population growth of 0.6% (2021-2025).

Brazil has historically seen reduced consumer purchasing power, contributing to increases in raw material prices for pet food products. These economic issues led to some consumers to become more cautious in controlling their expenditures affecting many sectors, however, particularly amongst the increasing number of single-person households, their was a preference to own a pet in lieu of having children. Additionally, many pet owners have increasing concern regarding their animals' quality of life, and are increasingly opting for services and products that mimic human offers (known as pet humanisation). These changes in consumer behaviour led to sales growth in mid-priced brands with premium positioning and the increased development of niche pet food/pet care products. Influenced by both slight economic recovery and consumption habit changes, pet food products in Brazil has become one of the top five markets globally in terms of retail value sales. Footnote 1

The Argentinian pet population was around 44.9 million, equivalent to 14.7 million households who are pet owners in 2020. The number of households owning a dog in Argentina were 10.3 million (70.0%), while households with a cat were 4.6 million (31.4%). Much like the trends in Brazil, the number of households owning pets in Argentina has increased at a slightly higher CAGR of 1.4% with it's population of pets increasing by 0.8% (2016-2020). The number of households with pets are expected to increase by a CAGR of 1.0%, equivalent to a population growth of 0.6% (2021-2025).

The weak economic landscape in Argentina has impacted volume growth and sales of pet care products across all categories. The pet food category wasn't affected much during Argentina's past economic crisis' in 2002 and 2009, since prepared pet food over homemade food just began to penetrate the market since then. Dogs and cats remain the favoured pets in Argentina, however, there is growth in demand for more exotic pets amongst pet owners that are living in urban small apartments in big cities like Buenos Aries, Cardoba and Rosario. Although economy pricing is important, the humanisation trend is also prevalent in Argentina despite unit price increases. Footnote 2

In 2020, the Venezuelan pet population was around 28.4 million, equivalent to 8.1 million households who are pet owners. During Venezuela's 2017-2018 economic crisis, which resulted in significantly reduced purchasing power, skyrocketing prices (inflation increasing as high as ~2,600%) and massive product/production shortages, pet owners found it extremely difficult to afford to feed their animals. This led to some dog and cat owners to abandon their pets, while some who consider their pets to be family members struggled to find ways to feed their animals with table scraps/leftovers, or often having to switch to smaller and cheaper pack sizes, brands and pet food product types. Footnote 3 The number of households owning pets has virtually remained the same between 2016-2020 at a CAGR of 0.02% with it's population of pets declining by −1.2% over this same period. Once the economy slowly begins to recover the number of households with pets are expected to increase by a CAGR of 3.2%, equivalent to a population growth of 2.3% (2021-2025).

| Country | Title (unit) | 2016 | 2020 | CAGR* (%) 2016-2020 | 2021 | 2025 | CAGR* (%) 2021-2025 |

|---|---|---|---|---|---|---|---|

| Brazil | Population ('000) | 206,162 | 212,583 | 0.8 | 213,985 | 218,986 | 0.6 |

| Households ('000) | 63,901 | 67,258 | 1.3 | 67,955 | 70,313 | 0.9 | |

| Argentina | Population ('000) | 43,484 | 44,884 | 0.8 | 45,185 | 46,302 | 0.6 |

| Households ('000) | 13,850 | 14,669 | 1.4 | 14,837 | 15,417 | 1.0 | |

| Venezuela | Population ('000) | 29,851 | 28,436 | −1.2 | 28,705 | 31,481 | 2.3 |

| Households ('000) | 8,075 | 8,083 | 0.02 | 8,242 | 9,345 | 3.2 | |

| Source: Euromonitor, 2021 *CAGR: Compound Annual Growth Rate | |||||||

| Country | Categorization type (unit) | 2016 | 2017 | 2018 | 2019 | 2020 |

|---|---|---|---|---|---|---|

| Brazil | Households owning a cat (%) | 20.1 | 20.4 | 20.8 | 21.0 | 21.2 |

| Households owning a cat ('000) | 12,831.5 | 13,236.0 | 13,648.0 | 13,976.5 | 14,257.1 | |

| Households owning a dog (%) | 48.4 | 48.6 | 48.8 | 48.9 | 49.0 | |

| Households owning a dog ('000) | 30,934.8 | 31,476.5 | 32,024.9 | 32,514.3 | 32,952.7 | |

| Argentina | Households owning a cat (%) | 30.4 | 31.1 | 31.3 | 31.3 | 31.4 |

| Households owning a cat ('000) | 4,207.4 | 4,392.1 | 4,489.6 | 4,562.4 | 4,639.6 | |

| Households owning a dog (%) | 69.8 | 70.3 | 70.0 | 70.1 | 70.0 | |

| Households owning a dog ('000) | 9,675.5 | 9,915.1 | 10,034.7 | 10,206.5 | 10,342.7 | |

| Source: Euromonitor, 2021 | ||||||

Trade of retail dog/cat food products in South America

In 2020, South American markets imported a total of US$313.3 million from the world in dog and cat food products, put up for retail sale. These dog/cat food products grew at a CAGR of 5.1% (2018-2020), and stood at a growth of 14.9% over the 2020/2019 period. Top countries for dog/cat pet food trade in this region included Chile (US$112.2 million), Colombia (US$67.8 million), and Uruguay (US$38.2 million). Although at a much smaller trade value than its top South American competitors, trailing in 10th ranking is Guyana, which has been growing at a 3-year CAGR of 22.3% and in 2020, reported a growth of 377.9% over 2019.

Selected countries: Argentina grew at a CAGR of 369.9%, followed by Brazil at a growth of 11.2% between 2018 and 2020, and Venezuela had a 14.0% growth (2019/2018). These three markets do not currently import pet food products from Canada, yet are considered emerging countries with great opportunity for trade growth into the introduction of Canadian brands since these countries have a high demand for pet food with a high population density in the number of households that own pets.

| Country | 2018 | 2019 | 2020 | CAGR* (%) 2018-2020 | % Growth difference (2020/19) |

|---|---|---|---|---|---|

| Total - dog/cat food, up for retail sale | 283,482,787 | 272,754,736 | 313,324,149 | 5.1 | 14.9 |

| 1. Chile | 112,645,404 | 92,872,235 | 112,235,983 | −0.2 | 20.8 |

| 2. Colombia | 46,506,272 | 53,314,139 | 67,773,570 | 20.7 | 27.1 |

| 3. Uruguay | 35,908,808 | 38,176,218 | 38,229,327 | 3.2 | 0.1 |

| 4. Peru | 33,886,388 | 33,046,942 | 34,532,905 | 1.0 | 4.5 |

| 5. Bolivia | 16,655,273 | 15,424,140 | 20,625,798 | 11.3 | 33.7 |

| 6. Ecuador | 11,572,400 | 13,395,167 | 12,260,197 | 2.9 | −8.5 |

| 7. Paraguay | 15,703,594 | 13,448,567 | 12,118,669 | −12.2 | −9.9 |

| 8. Brazil | 7,536,302 | 8,705,066 | 9,325,630 | 11.2 | 7.1 |

| 9. Argentina | 174,627 | 2,215,766 | 3,855,691 | 369.9 | 74.0 |

| 10. Guyana | 1,581,349 | 495,161 | 2,366,379 | 22.3 | 377.9 |

| 11. Venezuela (last available - 06/19) | 27,101 | 30,892 | 14.0 | n/a | |

| 12. Suriname (source: UN Comtrade) | 1,285,269 | 1,630,443 | 26.9 | n/a | |

| Source: Global Trade Tracker, 2021 *CAGR: Compound Annual Growth Rate n/a: not available | |||||

In 2020, South American markets often imported dog or cat food products from within, mainly from their neighbours in Argentina (29.8%) and Brazil (28.5%). Globally, the United States was their 3rd largest market for pet food at 2.2% with Colombia (48.5%) and Peru (31.0%) being their largest import partners. Meanwhile only Chile (1.9%), Colombia (0.5%) and Peru (3.7%) currently import dog/cat pet food from Canada, representing a total market share of 1.3%.

Selected markets: Brazil imported the most dog or cat food products at US$9.3 million from the world, importing mainly from Austria, Thailand, and Hungary in 2020. Argentina imported US$3.9 million mainly from Brazil, Austria, and France, while Venezuela met its demand through domestic supply and only imported US$30,892 (Jan-Jun'19) of dog/cat food products from the United states (97.3%), Spain, and Costa Rica.

| Rank | Country | Volume (metric tonnes) | Value (US$M) | Top import markets and value share % | Canada's value market share % | ||

|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | |||||

| Total - dog/cat food, up for retail sale | 227,223 | 286.6 | Argentina: 29.8 | Brazil: 28.5 | United States: 2.2 | Canada: 1.3 | |

| 1 | Chile | 84,284 | 112.2 | Argentina: 40.2 | United States: 20.0 | Brazil: 17.9 | Canada: 1.9 |

| 2 | Colombia | 41,513 | 67.8 | United States: 48.5 | Brazil: 35.9 | Mexico: 6.7 | Canada: 0.5 |

| 3 | Uruguay | 44,876 | 38.2 | Brazil: 59.0 | Argentina: 33.5 | United States: 4.2 | Canada: 0.0 |

| 4 | Peru | 25,568 | 34.5 | Argentina: 35.3 | United States: 31.0 | Brazil: 8.5 | Canada: 3.7 |

| 5 | Bolivia | 23,188 | 20.6 | Argentina: 56.3 | Brazil: 43.3 | France: 0.2 | Canada: 0.0 |

| 8 | Brazil | 6,056 | 9.3 | Austria: 26.1 | Thailand: 19.5 | Hungary: 17.9 | Canada: 0.0 |

| 9 | Argentina | 1,738 | 3.9 | Brazil: 72.4 | Austria: 22.5 | France: 4.6 | Canada: 0.0 |

| 11 | Venezuela[1] | 15 | 30,892 (actual)[1] | United States: 97.3 | Spain: 2.3 | Costa Rica: 0.4 | Canada: 0.0 |

| Source: Global Trade Tracker, 2021 1: last updated June 2019 | |||||||

Pet food retail sales in South America

Throughout South America, Brazil had the largest pet food market (includes dog, cat, bird, fish and small mammal/reptile) in terms of retail sales at US$4.4 billion (2,258,485.1 tonnes) in 2020. Colombia, Chile, Argentina, and Peru were the remaining top five retail markets in the pet food sector. Argentina had the largest historical CAGR at 31.2% between 2016-2020 with US$742.5 million (624,575.6 tonnes) in sales in 2020, and is expected to continue to have the highest growth at 28.8% (2021-2025), reaching US$3.1 billion (682,946.0 tonnes) in 2025.

Venezuela is also a large pet food market that registered a 5-year decline at a CAGR of −9.4%, however, is expected to show a growth of 9.3% increasing from retail value sales of US$102.0 million (57,576.1 tonnes) in 2020 to US$157.7million (76,368.5 tonnes) in 2025. All South American countries are expected to register a growth between the period of 2021 and 2025.

| Country | 2016 | 2020 | CAGR* (%) 2016-2020 | 2021 | 2025 | CAGR* (%) 2021-2025 |

|---|---|---|---|---|---|---|

| Total - pet food sales | 4,994.7 | 7,399.9 | 10.3 | 8,403.7 | 13,423.7 | 12.4 |

| 1. Brazil | 2,914.0 | 4,431.1 | 11.0 | 4,927.8 | 7,377.6 | 10.6 |

| 2. Colombia | 755.8 | 928.0 | 5.3 | 977.3 | 1,190.5 | 5.1 |

| 3. Chile | 637.5 | 822.5 | 6.6 | 873.4 | 1,077.3 | 5.4 |

| 4. Argentina | 250.5 | 742.5 | 31.2 | 1,110.9 | 3,060.8 | 28.8 |

| 5. Peru | 213.0 | 274.7 | 6.6 | 295.9 | 409.2 | 8.4 |

| 6. Venezuela | 151.1 | 102.0 | −9.4 | 110.3 | 157.7 | 9.3 |

| 7. Ecuador | 30.1 | 37.0 | 5.3 | 39.5 | 50.2 | 6.2 |

| 8. Uruguay | 21.0 | 32.6 | 11.6 | 36.2 | 51.5 | 9.2 |

| 9. Bolivia | 10.9 | 13.8 | 6.1 | 15.0 | 22.9 | 11.2 |

| 10. Paraguay | 8.1 | 12.0 | 10.3 | 13.0 | 19.1 | 10.1 |

| 11. Suriname | 1.4 | 2.1 | 10.7 | 2.7 | 4.7 | 14.9 |

| 12. Guyana | 1.3 | 1.6 | 5.3 | 1.7 | 2.2 | 6.7 |

| Source: Euromonitor, 2021 *CAGR: Compound Annual Growth Rate | ||||||

Retail sales breakdown in Brazil, Argentina, Venezuela

The dog and cat food category registered the highest retail sales throughout Brazil, Argentina and Venezuela, followed by bird food, fish food and small mammal/reptile pet food. Brazil leads the market for all categories, whereby sales for dog food totaled US$3.4 million (77.3%) and cat food sales were US$705.1 million (15.9%) and the remaining other pet food type sales were US$303.0 million (6.8%) in 2020. Between 2016 and 2020, all categories registered growth at CAGRs from 7.6 to 13.8% and is expected to grow at steady rates from 10.0 to 14.2% (2021-2025).

In 2020, Argentina followed with dog food sales of US$517.0 million (69.6%), cat food sales of US$185.0 million (24.9%), and other remaining pet food sales of US$40.5 million (5.5%). Between 2016 and 2020, all categories registered high growth at CAGRs from 25.7 to 31.9% and is expected to grow at steady rates from 23.1 to 29.3% (2021-2025).

Venezuela (modelled values) had approximate dog food sales of US$74.8 million (73.3%), cat food sales of US$26.3 million (25.8%), and remaining fish and bird food sales totalling US$1.0 million (0.9%) in 2020. Due to the economic crisis in Venezuela, all pet food categories registered a decline at CAGRs from −8.1% to −9.7% (2016-2020), yet is expected to begin to recover at growth rates from 0.0 to 10.2% (2021-2025).

| Country | Category | 2016 | 2020 | CAGR* (%) 2016-2020 | 2021 | 2025 | CAGR* (%) 2021-2025 |

|---|---|---|---|---|---|---|---|

| Total - pet food in Brazil | 2,914.0 | 4,431.2 | 11.0 | 4,927.8 | 7,377.6 | 10.6 | |

| Brazil | Dog food | 2,254.1 | 3,423.1 | 11.0 | 3,789.8 | 5,545.2 | 10.0 |

| Cat food | 460.5 | 705.1 | 11.2 | 798.1 | 1,283.3 | 12.6 | |

| Bird food | 97.2 | 162.9 | 13.8 | 185.9 | 316.4 | 14.2 | |

| Fish food | 88.1 | 121.2 | 8.3 | 133.5 | 201.6 | 10.9 | |

| Small mammal/reptile | 14.1 | 18.9 | 7.6 | 20.5 | 31.1 | 11.0 | |

| Total - pet food in Argentina | 250.6 | 742.5 | 31.2 | 1,111.0 | 3,060.8 | 28.8 | |

| Argentina | Dog food | 175.8 | 517.0 | 31.0 | 774.5 | 2,162.3 | 29.3 |

| Cat food | 61.1 | 185.0 | 31.9 | 278.0 | 762.5 | 28.7 | |

| Bird food | 11.0 | 32.4 | 31.0 | 46.8 | 109.0 | 23.5 | |

| Fish food | 2.5 | 7.6 | 32.0 | 10.9 | 25.0 | 23.1 | |

| Small mammal/reptile | 0.2 | 0.5 | 25.7 | 0.8 | 2.0 | 25.7 | |

| Total - pet food in Venezuela | 151.0 | 102.1 | −9.3 | 110.3 | 157.7 | 9.3 | |

| Venezuela | Dog food - modelled | 112.7 | 74.8 | −9.7 | 80.2 | 113.8 | 9.1 |

| Cat food - modelled | 36.8 | 26.3 | −8.1 | 29.1 | 42.9 | 10.2 | |

| Fish food - modelled | 1.2 | 0.8 | −9.6 | 0.8 | 0.8 | 0.0 | |

| Bird food - modelled | 0.3 | 0.2 | −9.6 | 0.2 | 0.2 | 0.0 | |

| Source: Euromonitor, 2021 *CAGR: Compound Annual Growth Rate | |||||||

| Country | Category | 2016 | 2020 | CAGR* (%) 2016-2020 | 2021 | 2025 | CAGR* (%) 2021-2025 |

|---|---|---|---|---|---|---|---|

| Total - pet food in Brazil | 2,069.1 | 2,258.5 | 2.2 | 2,356.4 | 2,647.0 | 2.9 | |

| Brazil | Dog food | 1,848.6 | 1,974.3 | 1.7 | 2,052.5 | 2,289.1 | 2.8 |

| Cat food | 178.6 | 236.9 | 7.4 | 256.5 | 312.1 | 5.0 | |

| Bird food | 42.2 | 44.5 | 2.5 | 44.6 | 42.7 | −1.1 | |

| Fish food | 1.5 | 1.6 | 2.8 | 1.7 | 1.9 | 3.0 | |

| Small mammal/reptile | 1.0 | 1.1 | 2.9 | 1.1 | 1.2 | 2.0 | |

| Total - pet food in Argentina | 642.2 | 624.6 | −0.7 | 633.9 | 682.9 | 1.9 | |

| Argentina | Dog food | 544.0 | 523.9 | −0.9 | 531.4 | 573.9 | 1.9 |

| Cat food | 90.4 | 93.3 | 0.8 | 95.2 | 102.2 | 1.8 | |

| Bird food | 7.6 | 7.1 | −1.6 | 7.0 | 6.5 | −1.8 | |

| Fish food | 0.192 | 0.183 | −1.2 | 0.184 | 0.192 | 1.0 | |

| Small mammal/reptile | 0.070 | 0.065 | −1.7 | 0.064 | 0.059 | −2.2 | |

| Total - pet food in Venezuela | 73.7 | 57.6 | −6.0 | 60.2 | 76.4 | 6.1 | |

| Venezuela | Dog food - modelled | 71.2 | 56.4 | −5.7 | 58.9 | 74.7 | 6.1 |

| Cat food - modelled | 2.0 | 0.955 | −17.3 | 1.0 | 1.4 | 8.2 | |

| Bird food - modelled | 0.358 | 183.5 | −15.4 | 0.184 | 0.200 | 2.2 | |

| Fish food - modelled | 0.069 | 31.9 | −17.5 | 0.032 | 0.035 | 2.2 | |

| Small mammal/reptile (modelled) | 0.035 | 15.0 | −19.1 | 0.015 | 0.016 | 2.4 | |

| Source: Euromonitor, 2021 *CAGR: Compound Annual Growth Rate | |||||||

In 2020, the largest sub-category in retail sales was dry dog and cat food throughout Brazil, Argentina and Venezuela at a value of US$4.5 billion, followed by wet dog/cat food (US$317.3 million), and dog/cat treats at US$156.0 million (mostly popular in Brazil). Brazil's sales for dry dog/cat food totaled US$3.7 billion (89.3%), followed by wet dog/cat food sales were US$298.9 million (7.2%), and dog/cat treat sales were US$143.3 million (3.5%) in 2020. All pet food categories had moderate growth between 2016 and 2020.

In 2020, Argentina sales for dry dog/cat food totaled US$671.7 million (95.7%), followed by wet dog/cat food sales were US$18.4 million (2.6%), and dog treat sales were US$11.9 million (1.7%) in 2020. All pet food categories registered high growth rates between 2016 and 2020.

Venezuela's modelled sales for dry dog/cat food totaled US$100.3 million (99.2%), followed by dog/cat treat sales at US$0.8 million (0.8%) in 2020. There were no wet food sales in Argentina. Most pet food categories had moderate historical declines, however, dog and cat treat sales were minimal and had the highest loss with CAGRs of −14.3% and −15.9%, respectively (2016-2020).

| Country | Sub-category | 2016 | 2017 | 2018 | 2019 | 2020 | CAGR* (%) 2016-2020 |

|---|---|---|---|---|---|---|---|

| Brazil | Total - dog food | 2,254.1 | 2,504.2 | 2,810.7 | 3,093.5 | 3,423.1 | 11.0 |

| Dry | 2,071.3 | 2,304.2 | 2,591.5 | 2,847.3 | 3,160.6 | 11.1 | |

| Treats | 79.8 | 92.6 | 105.1 | 122.8 | 136.8 | 14.4 | |

| Wet | 103.0 | 107.5 | 114.1 | 123.4 | 125.6 | 5.1 | |

| Total - cat food | 460.5 | 486.3 | 571.2 | 632.5 | 705.1 | 11.2 | |

| Dry | 369.2 | 385.6 | 437.7 | 471.9 | 525.3 | 9.2 | |

| Wet | 87.3 | 96.1 | 128.2 | 154.5 | 173.3 | 18.7 | |

| Treats | 4.0 | 4.6 | 5.3 | 6.1 | 6.5 | 12.9 | |

| Argentina | Total - dog food | 175.8 | 200.9 | 268.8 | 392.9 | 517.0 | 31.0 |

| Dry | 169.9 | 194.1 | 259.3 | 376.8 | 495.9 | 30.7 | |

| Treats | 3.7 | 4.3 | 5.7 | 9.0 | 11.9 | 33.9 | |

| Wet | 2.1 | 2.6 | 3.8 | 7.1 | 9.2 | 44.7 | |

| Total - cat food | 61.1 | 71.2 | 96.7 | 142.5 | 185.0 | 31.9 | |

| Dry | 58.9 | 68.3 | 92.6 | 135.5 | 175.8 | 31.4 | |

| Wet | 2.2 | 2.9 | 4.1 | 7.0 | 9.2 | 43.0 | |

| Venezuela | Total - dog food | 112.7 | 104.0 | 93.5 | 86.1 | 74.8 | −9.7 |

| Dry (modelled) | 111.5 | 102.9 | 92.5 | 85.3 | 74.1 | −9.7 | |

| Treats (modelled) | 1.3 | 1.1 | 1.0 | 0.8 | 0.7 | −14.3 | |

| Total - cat food | 36.8 | 33.8 | 31.0 | 28.2 | 26.3 | −8.1 | |

| Dry (modelled) | 36.6 | 33.6 | 30.8 | 28.0 | 26.2 | −8.0 | |

| Treats (modelled) | 0.2 | 0.2 | 0.2 | 0.1 | 0.1 | −15.9 | |

| Source: Euromonitor, 2021 *CAGR: Compound Annual Growth Rate | |||||||

Retail pricing trends in dog/cat food

In Brazil, consumers are more willing to pay premium prices for pet food products (mainly in the dry non-therapeutic category) over Argentina and Venezuela bringing a premium sales value of US$567.4 million (18.0%) in dry dog food and US$114.4 million (21.8%) in dry cat food products in 2020. Leading companies have raised their prices for pet food products with a high price per kilo in some categories such as wet food and therapeutic food. Less consumers are willing to pay this high price, however, despite economic difficulties their has been an increase in demand for product premiumisation driving growth also, in mid-priced brands. In Brazil, changes in consumption habits driven by the effect of pet humanisation, has helped product premiumisation to gain traction where premium product sales is expected to elevate faster in value over volume growth. With such changes in consumer behaviour, not only special premium foods benefited, but also the development of other niche products gained traction for hygiene and general wellbeing trends - notably cat litter, dietary supplements, pet cosmetics, vegan/natural food for animals with special needs and a rise in wet food sales and the creation of new snacks or foods aimed to simulate human food (chocolate, muffins and even beer). Footnote 1

In Argentina, as prepared pet food is now more common to feed their pets with a balanced diet, consumers remain increasingly price-sensitive and will often switch brands or trade down to opt for the most affordable options. Footnote 2 In 2020, the majority of sales were for 'Economy' food brands at a total value of US$247.3 million of dry dog food (49.9%) and US$87.0 million (49.5%) of dry cat food. Mid-priced food brands represented 30.3% in the dry dog food category and 29.5% in the dry cat food category, followed by premium food brands at the remaining 19.8% and 21.0%, respectively in 2020.

The latest financial crisis within Venezuela (2017), has driven manufacturers to raise their sales prices numerous times causing them to have to focus on producing more affordable economy dry dog and cat food products. With massive shortages in priority-consumption goods and manufacturers being unable to meet demand to restore production levels to those of 2013 due to rapidly rising costs, the entry of new domestic players and increased competition will be minimal. Footnote 3 Thus, Venezuela could be considered an emerging market for Canadian pet food manufacturers of economy-priced products that currently had a total modelled sales value of US$59.0 million in dog and cat food economy products in 2020.

| Country | Price category | 2016 | 2017 | 2018 | 2019 | 2020 | CAGR* (%) 2016-2020 |

|---|---|---|---|---|---|---|---|

| Brazil | Total - dry dog food | 2,071.3 | 2,304.2 | 2,591.5 | 2,847.3 | 3,160.6 | 11.1 |

| Mid-priced | 1,095.7 | 1,225.2 | 1,373.9 | 1,548.3 | 1,737.1 | 12.2 | |

| Economy | 639.8 | 702.6 | 788.6 | 810.0 | 856.2 | 7.6 | |

| Premium | 335.7 | 376.3 | 429.1 | 489.0 | 567.4 | 14.0 | |

| Non-therapeutic | 292.5 | 332.0 | 383.4 | 441.9 | 512.7 | 15.1 | |

| Therapeutic | 43.2 | 44.3 | 45.6 | 47.1 | 54.7 | 6.1 | |

| Total - dry cat food | 369.2 | 385.6 | 437.7 | 471.9 | 525.3 | 9.2 | |

| Mid-price | 245.2 | 264.4 | 309.1 | 337.6 | 378.3 | 11.4 | |

| Premium | 100.2 | 95.2 | 99.1 | 105.5 | 114.4 | 3.4 | |

| Non-therapeutic | 86.1 | 79.5 | 81.5 | 85.2 | 92.3 | 1.8 | |

| Therapeutic | 14.1 | 15.7 | 17.6 | 20.3 | 22.0 | 11.8 | |

| Economy | 23.9 | 26.0 | 29.5 | 28.9 | 32.6 | 8.1 | |

| Argentina | Total - dry dog food | 169.9 | 194.1 | 259.3 | 376.8 | 495.9 | 30.7 |

| Economy | 78.3 | 88.9 | 120.9 | 185.3 | 247.3 | 33.3 | |

| Mid-priced | 53.3 | 61.2 | 82.8 | 115.6 | 150.2 | 29.6 | |

| Premium | 38.3 | 44.0 | 55.6 | 75.9 | 98.3 | 26.6 | |

| Total - dry cat food | 58.9 | 68.3 | 92.6 | 135.5 | 175.8 | 31.4 | |

| Economy | 28.9 | 33.7 | 44.8 | 66.4 | 87.0 | 31.7 | |

| Mid-priced | 17.2 | 19.8 | 27.6 | 40.9 | 51.8 | 31.7 | |

| Premium | 12.8 | 14.8 | 20.1 | 28.2 | 37.0 | 30.4 | |

| Venezuela | Total - dry dog food | 111.5 | 102.9 | 92.5 | 85.3 | 74.1 | −9.7 |

| Economy (modelled) | 56.3 | 56.2 | 55.4 | 54.6 | 47.8 | −4.0 | |

| Mid-priced (modelled) | 54.1 | 45.7 | 36.3 | 29.9 | 25.6 | −17.1 | |

| Premium (modelled) | 1.1 | 1.0 | 0.8 | 0.7 | 0.6 | −14.1 | |

| Total - dry cat food | 36.6 | 33.6 | 30.8 | 28.0 | 26.2 | −8.0 | |

| Mid-priced (modelled) | 22.9 | 20.8 | 18.5 | 16.2 | 14.8 | −10.3 | |

| Economy (modelled) | 13.4 | 12.5 | 12.1 | 11.7 | 11.2 | −4.4 | |

| Premium (modelled) | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.0 | |

| Source: Euromonitor, 2021 *CAGR: Compound Annual Growth Rate | |||||||

In Brazil, the average price of dry dog pet food/treats range from US$2.35/kilogram to US$21.60/kilogram (78 brands). Prices of dry cat pet food/treats ranged from US$2.13/kilogram to US$43.96/kilogram (67 brands) and out of an 8 brand comparison, other bird/fish/small mammal/reptile pet food ranged from US$36.53/kilogram (bird food) to US$286.62/kilogram (fish food).

In Argentina, the average price of dry dog pet food/treats range from US$1.37/kilogram to US$12.55/kilogram (28 brands). Prices of dry cat pet food ranged from US$2.88/kilogram to US$8.88/kilogram (22 brands), and other pet food such as bird food had an average of US$3.89/kilogram (2 brands), fish food at US$259.80/kilogram (2 brands), and small mammal/reptile food at US$161.89/kilogram.

| Sub-category | Average price (US$/kilogram) | Sample size (number) |

|---|---|---|

| Total - dog food/treats price range (US$2.35 to 21.60/kilogram) | 78 | |

| Dog Treats | 21.60 | 10 |

| Premium Therapeutic Dry Dog Food | 10.29 | 12 |

| Premium Non-Therapeutic Dry Dog Food | 6.43 | 5 |

| Mid-Priced Wet Dog Food | 5.99 | 17 |

| Mid-Priced Dry Dog Food | 3.45 | 20 |

| Economy Dry Dog Food | 2.35 | 14 |

| Total - cat food/treats price range (US$2.13 to 43.96/kilogram) | 67 | |

| Cat Treats | 43.96 | 5 |

| Premium Therapeutic Wet Cat Food | 35.89 | 2 |

| Premium Non-Therapeutic Wet Cat Food | 29.05 | 7 |

| Premium Therapeutic Dry Cat Food | 16.31 | 8 |

| Premium Non-Therapeutic Dry Cat Food | 12.31 | 13 |

| Mid-Priced Wet Cat Food | 6.84 | 12 |

| Mid-Priced Dry Cat Food | 4.86 | 18 |

| Economy Dry Cat Food | 2.13 | 2 |

| Total - bird/fish/small mammal/reptile food price range (US$36.53 to 286.62/kilogram) | 8 | |

| Bird Food | 36.53 | 6 |

| Fish food | 286.62 | 1 |

| Small Mammal/Reptile Food | 117.96 | 1 |

| Source: Euromonitor, 2021 | ||

| Sub-category | Average price (US$/kilogram) | Sample size (number) |

|---|---|---|

| Total - dog food/treats price range (US$1.37 to 12.55/kilogram) | 28 | |

| Dog Treats | 12.55 | 3 |

| Premium Wet Dog Food | 9.21 | 4 |

| Premium Dry Dog Food | 6.02 | 5 |

| Mid-Priced Dry Dog Food | 2.83 | 8 |

| Economy Dry Dog Food | 1.37 | 8 |

| Total - cat food price range (US$2.88 to 8.88/kilogram) | 22 | |

| Premium Wet Cat Food | 8.88 | 2 |

| Premium Dry Cat Food | 8.25 | 8 |

| Mid-Priced Dry Cat Food | 4.54 | 5 |

| Economy Dry Cat Food | 2.88 | 7 |

| Total - bird/fish/small mammal/reptile food price range (US$3.89 to 161.89/kilogram) | 6 | |

| Bird Food | 3.89 | 2 |

| Fish food | 259.80 | 2 |

| Small Mammal/Reptile Food | 161.89 | 2 |

| Source: Euromonitor, 2021 | ||

Competitive landscape in the pet food sector

In 2020, leading companies (and top brand) in the pet food sector in Brazil included Mars Inc. (Folic) at 20.7% value share, Grandfood Industria e Comercio Ltda. (Golden) at 17.3%, and Nestlé SA (Dog Chow) at 11.0%. Private label pet food products held a 0.8% market value share.

In 2020, leading companies (and top brand) in the pet food sector in Argentina included Nestlé SA (Dog Chow) at 29.6% value share, Mars Southern Cone Alimentos Ltda (Pedigree) at 19.9%, and Petfood Saladillo SA (Tiernitos) at 9.2%. Private label pet food products held a 1.6% market value share.

According to Euromonitor, multinational players lead sales of premium pet food in Argentina and are also strong in mid-priced to economy offerings. Demands for premium products are higher than for cheaper pet food options and Argentinians prefer well-known products. Albeit, domestic players such as Pet Food Saladillo, Molino Chacabuco and Grupo Pilar are expected to better align their strategy by updating their packaging to try to change consumer perceptions of its brands and boost growth for national pet food offerings. Footnote 2

| Country | Company | Brand(s) | Market share (%) |

|---|---|---|---|

| Brazil | Mars Inc. | Folic, Trill, Pedigree, Whiskas, Royal Canin / (Veterinary Diet), Champ, Eukanuba, Kitekat | 20.7 |

| Grandfood Industria e Comercio Ltda. | Golden, Premier | 17.3 | |

| Nestlé SA | Dog Chow, Alpo, Kanina, Pro Plan, Friskies, Doguitos, Cat Chow, Deli-Dog, Revena | 11.0 | |

| Archer Daniels Midland Co | Max, Lider, Nero, Max Cat, Naturallis, Equilíbrio | 7.9 | |

| Mogiana Alimentos SA | Sabor & Vida, Herói, Guabi, Biriba, Fiel, Cat Meal, Top Cat | 4.8 | |

| Private labels | Private label | 0.8 | |

| Others | Others | 30.2 | |

| Total - market share | 92.7 | ||

| Argentina | Nestlé SA | Dog Chow, Pro Plan, Dogui, Gati, Cat Chow, Excellent, Friskies, Felix, Dog Menu | 29.6 |

| Mars Inc. | Pedigree, Royal Canin, Friskies, Performance, Eukanuba, Iams, Champ, Kitekat, Selection | 19.9 | |

| Petfood Saladillo SA | Tiernitos, Dog Selection, Pacho, Rosco, Mizzi Cat, Loyal Cat, Alimix | 9.2 | |

| Agroindustrias Baires SA | Voraz, Congo, Old Prince | 8.2 | |

| Metrive SA | Sabrositos, Sabro Food, Criadores, Balto | 5.7 | |

| Private labels | Private label | 1.6 | |

| Others | Others | 5.3 | |

| Total - market share | 79.5 | ||

| Source: Euromonitor, 2021 *CAGR: Compound Annual Growth Rate | |||

In 2020, Mars Incorporation within Brazil held the top market share for both the dog food category (14.1%) for its top Pedigree brand, as well as, in the cat food category (34.8%) for its top Whiskas brand. Other popular brands by top companies for dog food were Golden, Dog Chow, Premier and Royal Canin. Popular cat food brands in Brazil included Golden, Max Cat, Royal Canin, and Friskies.

Nestlé SA within Argentina held the top market share for both the dog food category (12.6%) for its top Dog Chow brand, as well as, in the cat food category (14.6%) for its top Cat Chow brand in 2020. Other popular brands by top companies for dog food were Pedigree, Royal Canin, Dogui, and Sabrositos. Popular cat food brands in Argentina included Gati, Whiskas, Pro Plan, and Performance.

| Country | Company | Dog brand | Market share (%) |

|---|---|---|---|

| Brazil | Mars Inc. | Pedigree | 14.1 |

| Grandfood Industria e Comercio Ltda. | Golden | 13.9 | |

| Nestlé SA | Dog Chow | 6.3 | |

| Grandfood Industria e Comercio Ltda. | Premier | 3.9 | |

| Mars Inc. | Royal Canin | 2.4 | |

| Private labels | Private label | 1.0 | |

| Others | Others | 36.2 | |

| Total - top brands | 77.8 | ||

| Argentina | Nestlé SA | Dog Chow | 12.6 |

| Mars Inc. | Pedigree | 11.3 | |

| Mars Inc. | Royal Canin | 6.7 | |

| Metrive SA | Dogui | 5.8 | |

| Nestlé SA | Sabrositos | 5.7 | |

| Private labels | Private label | 2.3 | |

| Others | Others | 4.0 | |

| Total - top brands | 48.4 | ||

| Source: Euromonitor, 2021 *CAGR: Compound Annual Growth Rate | |||

| Country | Company | Cat brand | Market share (%) |

|---|---|---|---|

| Brazil | Mars Inc. | Whiskas | 34.8 |

| Grandfood Industria e Comercio Ltda. | Golden | 20.2 | |

| Archer Daniels Midland Co | Max Cat | 7.9 | |

| Mars Inc. | Royal Canin | 7.4 | |

| Nestlé SA | Friskies | 4.4 | |

| Others | Others | 11.6 | |

| Total - top brands | 86.3 | ||

| Argentina | Nestlé SA | Cat Chow | 14.6 |

| Nestlé SA | Gati | 14.6 | |

| Mars Inc. | Whiskas | 10.4 | |

| Nestlé SA | Pro Plan | 7.9 | |

| Mars Inc. | Performance | 6.9 | |

| Private labels | Private label | 0.3 | |

| Others | Others | 7.6 | |

| Total - top brands | 62.3 | ||

| Source: Euromonitor, 2021 *CAGR: Compound Annual Growth Rate | |||

Covered to a lesser degree: In Brazil, Indústria e Comércio de Alimentos Desidratados Alcon Ltda. for its Alcon brand held the largest market share (19.8%) for sales in the bird food category in 2020. Other bird food companies in Brazil and their brand included Nutrópica Nutrição Especializada Ltda. (Nutropica) at 13.1% share and General Mills Inc. (Tori) at 8.9%; where the remaining 58.2% of the bird food market wasn't covered in 2020.

In Argentina, Distribuidora Nor SA for its Ibis brand and Nelsoni Ranch SA (Nelsoni Ranch) held market shares of 34.5% and 22.3%, respectively for sales in the bird food category in 2020. Notably, the remaining 43.2% of the bird food market wasn't covered in 2020.

| Country | Company | Bird food brand | Market share (%) |

|---|---|---|---|

| Brazil | Indústria e Comércio de Alimentos Desidratados Alcon Ltda | Alcon | 19.8 |

| Nutrópica Nutrição Especializada Ltda. | Nutropica | 13.1 | |

| General Mills Inc. | Tori | 8.9 | |

| Others | Others | 58.2 | |

| Total - top brands | 100.0 | ||

| Argentina | Distribuidora Nor SA | Ibis | 34.5 |

| Nelsoni Ranch SA | Nelsoni Ranch | 22.3 | |

| Others | Others | 43.2 | |

| Total - top brands | 100.0 | ||

| Source: Euromonitor, 2021 *CAGR: Compound Annual Growth Rate | |||

In Brazil, Spectrum Brands Holdings Inc. for its Tetra brand and Indústria e Comércio de Alimentos Desidratados Alcon Ltda (Basic) held market shares of 23.3% and 4.2%, respectively for sales in the fish food category in 2020. Private labels represented 1.6% market share. The remaining fish food market (70.9%) wasn't covered in 2020.

In Argentina, Shulet SA for its Shulet brand held the largest market share (73.2%) for sales in the fish food category in 2020. Other fish food companies in Argentina and their brand included Spectrum Brands Holdings Inc. (Tetra) at 2.1% share and Sera GmbH (Vipan) at 1.3%. The remaining 23.3% of the fish food market wasn't covered in 2020.

| Country | Company | Bird food brand | Market share (%) |

|---|---|---|---|

| Brazil | Spectrum Brands Holdings Inc. | Tetra | 23.3 |

| Indústria e Comércio de Alimentos Desidratados Alcon Ltda. | Basic | 4.2 | |

| Private label | Private label | 1.6 | |

| Others | Others | 70.9 | |

| Total - top brands | 100.0 | ||

| Argentina | Shulet SA | Shulet | 73.2 |

| Spectrum Brands Holdings Inc. | Tetra | 2.1 | |

| Sera GmbH | Vipan | 1.3 | |

| Others | Others | 23.3 | |

| Total - top brands | 100.0 | ||

| Source: Euromonitor, 2021 *CAGR: Compound Annual Growth Rate | |||

In Brazil, the Alcon brand manufactured by Indústria e Comércio de Alimentos Desidratados Alcon Ltda. held a sales market share of 47.8% in the small mammal/reptile food category in 2020. A remaining market share of 52.2% wasn't covered in this food category.

In Argentina, Distribuidora Nor SA for its Ibis brand and Nelsoni Ranch SA (Nelsoni Ranch) held market shares of 41.3% and 25.2%, respectively for sales in the small mammal/reptile food category in 2020. A remaining 33.6% of the small mammal/reptile market wasn't covered in 2020.

| Country | Company | Pet food brand | Market share (%) |

|---|---|---|---|

| Brazil | Indústria e Comércio de Alimentos Desidratados Alcon Ltda. | Alcon | 47.8 |

| Others | Others | 52.2 | |

| Total - top brands | 100.0 | ||

| Argentina | Distribuidora Nor SA | Ibis | 41.3 |

| Nelsoni Ranch SA | Nelsoni Ranch | 25.2 | |

| Others | Others | 33.6 | |

| Total - top brands | 100.0 | ||

| Source: Euromonitor, 2021 *CAGR: Compound Annual Growth Rate | |||

Retail distribution channels of pet food (off-trade)

Brazil: With the premiumisation trend being strong in the Brazilian pet food sector, consumers are increasingly looking for personalized products and services that meet their special pet care needs. To meet these more demanding consumers for a larger diversity of product offerings, pet superstores and competitive warehouse clubs such as Atacadäo and Assaí have continued to gain space over grocery hypermarket retailers. Footnote 1 In 2020, non-grocery specialists represented 66.9% market share with growth in pet superstores (10.7%), while mixed retailers such as warehouse clubs had a value share of 4.4% and grocery retailers (includes hyper/supermarkets) represented 21.1%.

Consumers also, want the practicality of reducing or eliminating the number of visits to different outlet types. The consumers who prefer grocery retailers are those who do not look for personalization, such as generally low-income consumers, who demand basic products at reduced prices per kilo. While supermarkets have lost share in Brazil, the e-commerce channel have grown significantly over the past two years mostly due to their main pet superstore websites such as those owned by Petz and Cobasi and online-exclusive shops (PetLove). The digital delivery app such as Rappi is becoming a way to shop within the retail e-commerce pet food channel, as well. Footnote 1

| Outlet type | Market share % in 2019 | Market share % in 2020 |

|---|---|---|

| Store-based retailing | 95.3 | 92.4 |

| Grocery retailers | 21.2 | 21.1 |

| Modern grocery retailers (hyper/supermarkets) | 15.5 | 15.4 |

| Traditional grocery retailers | 5.6 | 5.6 |

| Mixed retailers (warehouse clubs) | 4.5 | 4.4 |

| Non-grocery specialists | 69.6 | 66.9 |

| Pet superstores | 9.9 | 10.7 |

| Pet shops | 51.1 | 47.6 |

| Other non-grocery specialists | 8.5 | 8.5 |

| Non-store retailing (e-commerce) | 3.0 | 6.0 |

| Non-retail channels (veterinary clinics) | 1.7 | 1.6 |

| Total - distribution channels for pet food | 100.0 | 100.0 |

| Source: Euromonitor, 2021 | ||

Argentina: Contrasting Brazil in 2020, traditional grocery retailers at a market share of 48.8% are the main retailers for pet care products in Argentina primarily in the form of forrajerias retailers. To increase profit sales, many forrajerias owners have transformed their stores into pet stores in order to offer a larger array of pet products, along with specialized knowledge. Non-retail veterinary clinics (21.5%), along with non-grocery specialist pet shops (5.9%) are also essential retailers in Argentina for pet care outlets being the preferred choice to gain specialized advice, insights and knowledge.

E-commerce (5.7%) is slowly rising in Argentina mostly for bulk pet food products offered at lower prices and for the convenience of not having to carry heavy dog food packaging products. This growth is also driven by leading pet stores (Puppis and MisPichos) who vamped up their websites and are encouraging online sales through online-only discounts and free online consultation incentives. Footnote 2

| Outlet type | Market share % in 2019 | Market share % in 2020 |

|---|---|---|

| Store-based retailing | 73.5 | 72.8 |

| Grocery retailers | 67.5 | 66.9 |

| Modern grocery retailers (hyper/supermarkets) | 18.9 | 18.0 |

| Traditional grocery retailers | 48.6 | 48.8 |

| Non-grocery specialists (pet shops) | 6.0 | 5.9 |

| Non-store retailing (e-commerce) | 2.7 | 5.7 |

| Non-retail channels (veterinary clinics) | 23.8 | 21.5 |

| Total - distribution channels for pet food | 100.0 | 100.0 |

| Source: Euromonitor, 2021 | ||

Product launch and trend analysis in selected markets

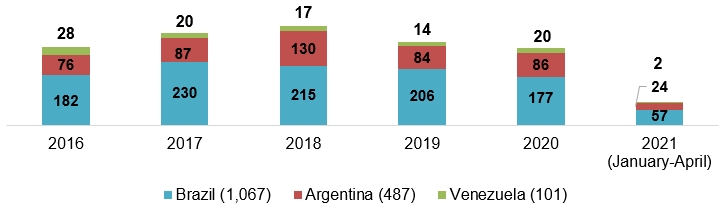

Mintel indicates that there were 1,655 pet food products launched (including new variety/range extension, packaging, formulation or relaunched) in Brazil (64.5%), Argentina (29.4%), and Venezuela (6.1%) between the period of January 2016 and April 21st, 2021.

Description of above image

| Country | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 (January-April) | Total |

|---|---|---|---|---|---|---|---|

| Brazil | 182 | 230 | 215 | 206 | 177 | 57 | 1067 |

| Argentina | 76 | 87 | 130 | 84 | 86 | 24 | 487 |

| Venezuela | 28 | 20 | 17 | 14 | 20 | 2 | 101 |

Source: Mintel, 2021

Brazil

According to Mintel, top parent companies launching dog and cat pet food products in Brazil from January 2016 to April 21, 2021 were Nestlé/Nestlé Nordeste Alimentos e Bebidas (153) products, Mars Inc. (87), Petitos Indústria e Comércio de Produtos para Animais (78), Guabi (71), and Mogiana Alimentos (69). Top brands include Sabor & Vida (19), Kelco Keldog (Dental) (26), Affinity Faro (14), Whiskas (13) and Purina Friskies (11). New brands in the Brazilian market include FVO Katita Dog (meat flavoured for puppies), Purina Felix Fantastic (salmon and meat flavoured cat food) Mix, Pet Food Solution Qualiday (meat and rice flavour for adult cats), and Fórmula Natural (pumpkin, coconut and quinoa flavored dog biscuits).

The fastest growing flavours in Brazilian pet food products were salmon, barbecue, cereal, vegetable, flax/linseed, and unflavoured/plain (Q2-2021/Q2-2019). New ingredients included carrot pulp, Aberdeen angus beef, sesame seed oil, peanut butter, cherry, soursop, savia, and lamb chop. Lastly, top growing claims were joints, bones and muscles (+400%), low/no/reduced transfat (+150%), and functional - weight and muscle gain (+100%), while declining claims (−100%) included added calcium, low/no/reduced glycemic, functional - slimming, low/no/reduced lactose, and high/added fibre.

In Brazil, dog snacks and treats was the largest sub-category with 532 new pet food product launches (49.9%) over the 6-year period. Whereby, the dry dog food sub-category launched 195 new products (18.3%), followed by wet cat food at 104 new products (9.7%).

| Sub-category | Top 50 brands launched (product item count) | Number of products in category |

|---|---|---|

| Dog snacks and treats | Kelco Keldog/dental (22), Petitos/Petitos Delícias do Chef (13), Origem Natural (10), PetDog (9), Upper Dog (8), Purina Doguitos (8), Pets du Monde Cannix (7), Mastig (7), 8 in1 (6), Luopet Snacks Dog Menu Baked (6), The French Co. (6), Pethy Group Zoo Prime Ossyto (5), Petz (5), Snack Show (5), Prabicho Petiscão (5), Barkeria (5), Cadet Gourmet (5), Baw Waw (4), Simple Dog (4), Bone Apettit (4), Padaria Pet (3), Dr. Stanley All Love (3), XisDog (3), Qualitá (2), PremieRpet Premier Gourmet (2), Affinity Faro (1), Carrefour (1), New Dog (1) | 532 |

| Dry dog food | Pedigree/Vital Pro (8), Sabor & Vida (6), Purina Dog Chow (6), Baw Waw/Natural Pro (5), Affinity Faro (4), Balance (4), Affinity Ultima/Affinity Guabi Natural (Grain Free) (4), Purina Pro Plan (3), Barão (3), Qualitá (2), Simple Dog (2), Dr. Stanley All Love (2), Carrefour (1), New Dog (1) | 195 |

| Wet cat food | Whiskas (9), Purina Friskees (8), Royal Canin Feline Care Nutrition (5), Sheba Cortes Selecionados (5), Sabor & Vida (4), Purina Pro Plan (3), Affinity Faro/Affinity Guabi Natural Grain Free (3), Pet Delícia (2), Padaria Pet (2), Qualitá (2), PremieRpet Premier Gourmet (2), Purina Cat Chow (2), Carrefour (1), Affinity Ultima (1), Baw Waw (1) | 104 |

| Wet dog food | Sabor & Vida (6), Pet Delícia (6), Affinity Faro/Ultima/Affinity Guabi Natural Grain Free (5), Kelco Keldog (4), Purina Dog Chow/Extra Life (4), Pedigree/Vital Pro (4), New Dog (3), Baw Waw (2), Purina Pro Plan (2), Qualitá (2), PremiRpet Premier Gourmet (2), Carrefour (2), XisDog (2), Padaria Pet (1), Bone Apettit (1) | 103 |

| Dry cat food | Affinity Faro/Ultima/Affinity Guabi Natural (Grain Free) (9), Purina Friskies/Purina Pro Plan/Purina Cat Chow (8), Royal Canin Feline Health Nutrition (5), Sabor & Vida (3), Baw Waw/ Natural Pro (3), Royal Canin Feline Care Nutrition (3), Whiskas (2), Qualitá (1), Barão (1) | 197 |

| Cat snacks and treats | Baw Waw/Gatos (4), Whiskas (2), Padaria Pet (2), Petitos/Delícias do Chef (2) | 136 |

| Total sample size | 1,067 | |

| Source: Mintel, 2021 | ||

Argentina

Top parent companies launching dog and cat pet food products in Argentina from January 2016 to April 21, 2021 were Nestlé/Nestlé Nordeste Alimentos e Bebidas (98) products, Mars Inc. (91), MasterFoods (46), Royal Canin (40), and GoloCan (37). Top brands include GoloCan (30), Raza (24), Pet's Class (20), Whiskas (19) and Natuplus (11). New brands in the Argentinian market include Core (chicken and rice super premium dry food for small adult dogs), Sieger Super Premium Criadores (complete balanced food for dogs), Goodies Premium (dry food for adult dogs), and Iams Proactive Health (healthy kitten kibbles with chicken).

The fastest growing flavours in Brazilian pet food products were rice, chicken, and meat - with little growth in salmon and seafood flavours and unflavoured/plain declining by −25.0% (Q2-2021/Q2-2019). New ingredients included artificial smoke flavour, lysine hydrochloride, trimethylglycine, zinc monomethionine, spirulina, soybean germ, isoflavones, corn semolina, and smoke extract. Lastly, top growing claims were free from added/artificial flavourings (+200%), added calcium (+200%), and premium (+100%), while declining claims (−100%) included high/added fibre, cobranded, functional - heart and cardiovascular system, and functional - urinary tract.

In Argentina, dog snacks and treats was the largest sub-category with 191 new pet food product launches (39.2%) over the 6-year period. Whereby, the dry dog food sub-category launched 115 new products (23.6%), followed by dry cat food at 76 new products (15.6%).

| Sub-category | Top 50 brands launched (product item count) | Number of products in category |

|---|---|---|

| Dog snacks and treats | GoloCan (30), Pet's Class (12), Natuplus (11), Proetto Dr. Zoo (10), Mon Ami (8), Vaquero (7), Can Biscotti (7), Purina Dog Chos Abrazzos (6), Pet's Fun! (6), Zoo (5), Mister Dog's (5), Pedigree DentaStix (5), Pet CanCat (5), Vexp Vision Exp. Angus Natural (5), Raza (4), Carrefour (4), X-Limp Pets (4), All Pet's (4), Pet and Pop (4), Ímpetu Dog (4), Cross+Pro (3) | 191 |

| Dry dog food | Purina Dog Chow Salud Visible Extra Life/Purina Pro Plan/Purina Dog Chow (11), Royal Canin Breed/Size Health Nutrition (7), Raza (6), Metrive Sabrositos (5), Pedigree Vital Protection (5), Tiernitos Selección (5), Eukanuba (4), Baires Kongo/ Kongo (4), Patagonia (3), Voraz (2), Mon Ami (1), King Food (1), VitalCan Complete (1) | 115 |

| Dry cat food | Raza (11), Whiskas (11), Purina Cat Chow/Purina Gati Sabores Caseros (9), Baires Kongo/Kongo Gourmet Healthy Living (7), VitalCan Complete/Balanced (3), GEPSA Pet Foods Mizzi Cat (3), Patagonia (1), Metrive Sabrositos (2), Royal Canin Feline Health Nutrition (2), Voraz (2) | 76 |

| Wet dog food | Royal Canin Size/Breed/Canine Health Nutrition/Royal Canin Veterinary Diet (14), Pedigree (8), Purina Dog Chow/Vida Sana/Purina ProPlan (7), Pet's Class (3), Carrefour (3), VitCan Complete/Balanced (3), King Food (2), Raza (1), Eukanuba (1) | 49 |

| Wet cat food | Purina Cat Chow/Purina Felix/Purina Fancy Feast (17), Whiskas (8), Pet's Class (5), Royal Canin Feline Health Nutrition (4), Carrefour (3), King Food (2), Raza (1), VitalCan Complete (1) | 46 |

| Cat snacks and treats | GoloMiau (6), Dr. Zoo (3), Raza (1) | 10 |

| Total sample size | 487 | |

| Source: Mintel, 2021 | ||

Venezuela

Top parent companies launching dog and cat pet food products in Venezuela from January 2016 to April 21, 2021 were Nestlé/Nestlé Purina PetCare (42) products, Mars Inc. (10), MasterFoods (6), Alimentos Polar Comercial (5), and Foshan Phoenix Pet Products (5). Top brands include Purina Friskies (7), Woof! (6), Bruno Pet Gourmet (5), Purina Cat Chow (4) and Gnawlers (4). A new brand introduced into the Venezuelan market by Mars Inc. in December (2020) is Pedigree Homestyle Meals (prime rib, rice and vegetable flavor in gravy food for dogs).

Pet food flavours with declining growth (−100.0%) in Venezuela were unflavoured/plain, salmon, fish, trout, and smoke- with little growth in beef flavoured products (Q2-2021/Q2-2019). New ingredients included salmon meal, tuna meal, poultry protein, parboiled rice, l-glycine, modified starches, iron dioxide, pig liver, green bean and beef lung. As there is little growth in new pet food launches in Venezuela, top declining trending claims (−100%) included low/no/reduced allergen, functional - urinary tract, pet - adult, functional - digestion, and vitamin/mineral fortified.

In Venezuela, dog snacks and treats was the largest sub-category with 33 new pet food product launches (32.7%) over the 6-year period. Whereby, the dry dog food sub-category launched 26 new products (25.7%), followed by dry cat food at 19 new products (18.8%).

| Sub-category | Top 50 brands launched (product item count) | Number of products in category |

|---|---|---|

| Dog snacks and treats | Woof! (6), Gnawlers (4), Kantal Super Galletas (3), Maskosnacks (2), Totti Pets (2), Panchetas (2), Green Dogs (2), Bruno Pet Gourmet (1), Pro Pac (1), Chiguau (1), Dong Da Smily Pet (1), Beefy Snack's (1), Athos (1), Perro Gourmet (1), Can Mordidas (1) | 33 |

| Dry dog food | Purina Dog Chow Digestión Sana = Vida Sana/Purina Dog Chow/Cachorros/Purina K-Nina (Gold)/Purina Pro Plan Optimal Nutrition (11), Pedigree Vital Protection (3), Dogourmet/Adultos/Cachorros (4), Italcol Chunky (2), AllPets Dog Dog/Pro (2), Naturacan (1), Nutrion (1), Protinal Protican (1) | 26 |

| Dry cat food | Purina Cat Chow/ Purina Friskies Selección Especial (5), Whiskas/Gatitos (5), Diamond (2), Cat Chef Mix (1), Nutrion Gatos (1), Raza Supercat Deli (1), Happy One (1), Protinal Proticat (1) | 19 |

| Wet cat food | Purina Friskies (7), 9 Live (2), Lambon (1) | 10 |

| Wet dog food | Purina Alpo Prime Cut/Purina Pro Plan Focus (3), Bruno Pet Gourmet (3), Pedigree/ Homestyle Meals(2) | 8 |

| Cat snacks and treats | Purina Whisker Lickin's (1), Bruno Pet Gourmet (1), Maskosnacks (2) | 5 |

| Total sample size | 101 | |

| Source: Mintel, 2021 | ||

Product examples

Super Premium Snacks for Dogs with Spearmint, Carrot & Copaiba Oil

Source: Mintel, 2021

| Company | Nats Comércio de Produtos para Animais |

|---|---|

| Brand | Nats Oral Fresh |

| Sub-category | Dog snacks and treats |

| Country | Manufactured in Brazil, not imported |

| Related claims | No additives/preservatives, premium, anti-bacterial, breath-freshening, teeth and tartar prevention, GMO free |

| Store name | Semeve Pet Center, specialist retailer |

| Launch type | New product |

| Date published | March 2021 |

| Price in US dollars | 2.57 |

This premium blend is said to be the perfect balance of flavour, with natural and highly nutritious ingredients that provide the maximum sense of well-being for pets. This natural food for small breed dogs is formulated with rosemary extract and contains no colorings or transgenic ingredients. It is recommended for daily oral hygiene and helps to keep fresh breath and fight the accumulation of tartar and bacterial plaque.

Meat & Rice Flavored Food for Adult Cats

Source: Mintel, 2021

| Company | Pet Food Solution |

|---|---|

| Brand | Pet Food Solution Qualiday |

| Sub-category | Dry cat food |

| Country | Manufactured in Brazil, not imported |

| Related claims | No additives/preservatives, premium, vitamin/mineral fortified, functional – skin and coat/digestion/urinary tract |

| Store name | Perfumaria Goya, specialist retailer |

| Launch type | New packaging |

| Date published | February 2021 |

| Price in US dollars | 8.24 |

This premium cat food is made from natural raw materials and has been formulated by those who understand the importance of nutrition for quality of life and well-being. It features hairball control with a combination of high-quality fibers, which favors intestinal flux, facilitating the elimination of hairballs; high-quality proteins that provide ideal energy; balanced content of fatty acids, omegas 3 and 6, and biotin to help in the maintenance of beautiful skin and coat; a combination of mannan oligosaccharides and fructooligosaccharides that favors the absorption of nutrients and intestinal balance; yucca extract that helps reduce the odor of feces; and phosphoric acid that contributes for a balanced pH and the prevention of kidney stones.

Complete Balanced Food for Dogs

Source: Mintel, 2021

| Company | Alican |

|---|---|

| Brand | Sieger Súper Premium Criadores |

| Sub-category | Dry dog food |

| Country | Manufactured in Argentina, not imported |

| Related claims | Premium, vitamin/mineral fortified, functional – joints/bones and muscles/teeth and tartar/skin and coat/digestion, prebiotic, pet – adult, junior |

| Store name/type | Puppis Pet Supplies, specialist retailer |

| Launch type | New product |

| Date published | February 2021 |

| Price in US dollars | 8.75 |

This premium product is a complete balanced food of high performance cooked by extrusion, which can be used in all stages of the dog's life. In puppies, it is said to provide the necessary nutrients for optimal growth, aiding the development of strong muscles, firm ligaments and providing a lot of vitality. In adults, it is said to provide a balanced and natural diet of high digestibility and an adequate ratio between energy and proteins, helping to maintain a shiny coat, healthy teeth and an excellent physical condition. This dog food contains vitamin A, omega 3, and omega 6, which help to improve skin and hair; organic zinc bound with methionine to strengthen its absorption and assimilation; prebiotics (MOS and FOS), which help with proper functioning of the digestive tract; yucca extract, which helps to reduce odors in droppings; and beet pulp, which favors the formation of firm stools.

Healthy Kitten Kibbles with Chicken

Source: Mintel, 2021

| Company | MasterFoods |

|---|---|

| Brand | Iams Proactive Health |

| Sub-category | Dry cat food |

| Country | Manufactured in the Argentina, not imported |

| Related claims | Added calcium, premium, vitamin/mineral fortified, functional – brain and nervous system/ eyesight/joints, bones and muscles/immune system/ digestion, prebiotic, pet – junior |

| Store name/type | Puppis Pet Supplies INTL. SA, specialist retailer |

| Launch type | New product |

| Date published | March 2021 |

| Price in US dollars | 6.35 |

The premium complete and balanced food features small-sized kibbles for small mouths, designed to be easy to swallow, and is said to promote: cognitive development, with omega 3 DHA for learning; healthy eyesight development, with taurine; strong immune system, with vitamin E; healthy digestion, with prebiotics and beetroot pulp; and strong bones with essential minerals and calcium. It features chicken protein as the first ingredient, is rich in milk nutrients, and is suitable for kittens aged from one to 12 months.

Super Premium Nutra Nuggets Maintenance Formula for Adult Cats

Source: Mintel, 2021

| Company | Diamond Pet Foods |

|---|---|

| Brand | Diamond |

| Sub-category | Dry cat food |

| Country | Manufactured in the United States, market Venezuela |

| Related claims | Premium, vitamin/mineral fortified, wholegrain, low/no/reduced allergen, functional – digestion/ other, pet – adult |

| Store name/type | Inversiones El Hogar de la Mascot's, supermarket |

| Launch type | New product |

| Date published | August 2020 |

This premium product is designed to provide longevity, health, and wellbeing for adult cats. It is formulated with high quality nutrients, including omega 3 fatty acids, and features controlled magnesium and balanced pH; combines high quality chicken, egg protein, highly digestible chicken fat, and wholegrains formulated and balanced with the exact quality of vitamins and minerals to provide high levels of nutrients which help to maintain normal weight, energy, and good health; high digestibility for less waste with digestible proteins and wholegrains; beet pulp, which is considered a premium source of fiber and helps to maintain normal gastrointestinal health, and omega fatty acids, including omega 6, which is considered an essential fatty acid for dogs and cats, and omega 3, which is also important for maintaining health. The product is preserved with natural tocopherols, a form of vitamin E, and is free from wheat, soy, BHA and BHT.

Super Premium Nutra Nuggets

Source: Mintel, 2021

| Company | Diamond Pet Foods |

|---|---|

| Brand | Diamond |

| Sub-category | Dry cat food |

| Country | Manufactured in the United States, market Venezuela |

| Related claims | Premium, low/no/reduced allergen, functional – skin and coat/digestion, pet – adult, junior |

| Store name/type | Inversiones El Hogar de la Mascot's, supermarket |

| Launch type | New product |

| Date published | July 2020 |

| Price in US dollars | 19.60 |

This professional product for cats and kittens features: natural fibre to support digestion; balanced nutrition formulation; active lifestyle formulation that is claimed to be perfect for active adult cats; and fatty acid nutrition with a blend of omega 6 and omega 3 fatty acids for optimum skin and coat health. It is free from soy and wheat.

For more information

The Canadian Trade Commissioner Service:

International Trade Commissioners can provide Canadian industry with on-the-ground expertise regarding market potential, current conditions and local business contacts, and are an excellent point of contact for export advice.

- Find a Trade Commissioner

More agri-food market intelligence:

International agri-food market intelligence

Discover global agriculture and food opportunities, the complete library of Global Analysis reports, market trends and forecasts, and information on Canada's free trade agreements.

Agri-food market intelligence service

Canadian agri-food and seafood businesses can take advantage of a customized service of reports and analysis, and join our email subscription service to have the latest reports delivered directly to their inbox.

More on Canada's agriculture and agri-food sectors:

Canada's agriculture sectors

Information on the agriculture industry by sector. Data on international markets. Initiatives to support awareness of the industry in Canada. How the department engages with the industry.

For additional information on an upcoming Trade Show, please contact:

Ben Berry, Deputy Director

Trade Show Strategy and Delivery

Agriculture and agri-food Canada

ben.berry@agr.gc.ca

Resources

- Euromonitor, 2021. Data statistics (2016-2025)

- Euromonitor, May 2020. Country report: Pet Care in Argentina (pre-COVID-19 report)

- Euromonitor, May 2020. Country report: Pet Care in Brazil (pre-COVID-19 report)

- Euromonitor, May 2018. Country Report: Pet Care in Venezuela (pre-COVID-19 report)

- Global Trade Tracker, 2021

- Mintel Global New Products Database, 2021

Sector Trend Analysis – Pet food in South America and selected markets: Brazil, Argentina, Venezuela

Global Analysis Report

Prepared by: Erin-Ann Chauvin, Market Analyst

© Her Majesty the Queen in Right of Canada, represented by the Minister of Agriculture and Agri-Food (2021).

Photo credits

All photographs reproduced in this publication are used by permission of the rights holders.

All images, unless otherwise noted, are copyright Her Majesty the Queen in Right of Canada.

To join our distribution list or to suggest additional report topics or markets, please contact:

Agriculture and Agri-Food Canada, Global Analysis1341 Baseline Rd, Tower 5, 3rd floor

Ottawa ON K1A 0C5

Canada

Email: aafc.mas-sam.aac@agr.gc.ca

The Government of Canada has prepared this report based on primary and secondary sources of information. Although every effort has been made to ensure that the information is accurate, Agriculture and Agri-Food Canada (AAFC) assumes no liability for any actions taken based on the information contained herein.

Reproduction or redistribution of this document, in whole or in part, must include acknowledgement of agriculture and agri-food Canada as the owner of the copyright in the document, through a reference citing AAFC, the title of the document and the year. Where the reproduction or redistribution includes data from this document, it must also include an acknowledgement of the specific data source(s), as noted in this document.

Agriculture and Agri-Food Canada provides this document and other report services to agriculture and food industry clients free of charge.

Source: https://agriculture.canada.ca/en/international-trade/market-intelligence/reports/sector-trend-analysis-pet-food-south-america-and-selected-markets-brazil-argentina-venezuela

{kind=link}

Postar um comentário for "Value of Brazilian Beef Sales to Ei"